Industry Trends

Largest Transactions Closed

- Target

- Buyer

- Value($mm)

Advised Western Milling in their sale to the Western Milling ESOP Trust

Last updated:

Consumer & Retail M&A continued to recalibrate in Q1 2026, with fewer deals but steady buyer appetite for high-quality assets. Valuations stayed disciplined on earnings, while revenue-centric pricing strengthened for businesses with durable demand and clear differentiation. Strategic acquirers remained the primary consolidators, and sponsors were selective—leaning into take-privates and platform builds where operational improvement and pricing flexibility can drive returns. Overall, capital concentrated around scaled brands with pricing power and category leadership.1

According to Joe Anto, Managing Director at PCE "Consumer & Retail M&A continues to narrow around high-conviction plays as volume declines but revenue multiples expand, rewarding targets with real pricing power and category leadership. The surge in take-privates and cross-border interest tells us capital is finding opportunities in this market, it's just being deployed with far more precision than in prior cycles."

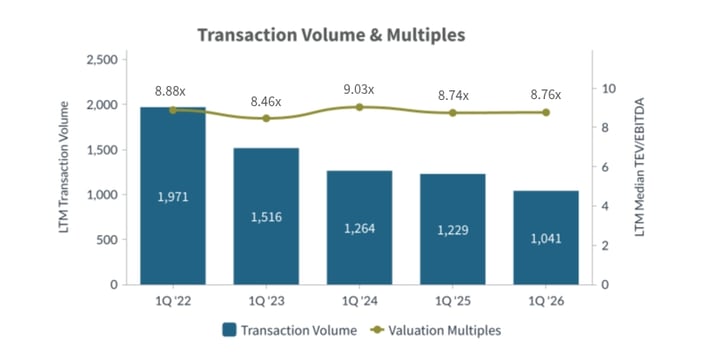

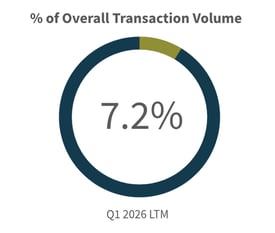

Deals totaled 1,041 on an LTM basis, down from 1,229 a year earlier, as the sector continued its multi-year volume normalization. Valuations showed divergence, with LTM median EBITDA multiples holding at 8.76x while revenue multiples expanded to 1.33x from 1.22x. Strategic buyers concentrated on targets offering category leadership and top-line resilience, while financial sponsors leaned into take-privates and hospitality investments where operational repositioning and pricing flexibility support near-term value creation. 1

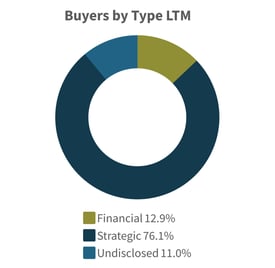

Strategic Acquirers: Strategic buyers represented 76.1% of LTM deals, maintaining their dominant role as the primary consolidators in Consumer & Retail. Activity was concentrated in hospitality, automotive retail, and experiential entertainment as acquirers pursued assets with embedded consumer demand and category density.1

Financial Buyers: Financial sponsors accounted for 12.9% of LTM deals, deploying capital into take-privates and yield-oriented hospitality acquisitions. Sponsor selectivity persisted as underwriting increasingly stressed recession sensitivity, tariff pass-through capacity, and consumer elasticity risk.1

Consumer & Retail dealmaking in Q1 2026 remains selective following a 2025 that saw the sector record a 7% decline in overall deal activity and a 29% drop in retail M&A by value. Buyer confidence has strengthened, however, with both strategic and financial sponsors increasingly pursuing high-conviction opportunities as portfolio precision and category sharpening define the current deal environment.2 4

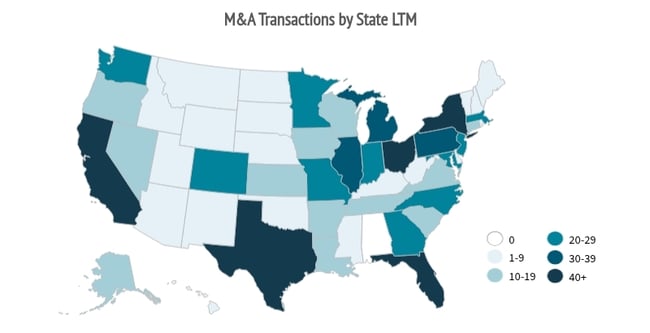

Top U.S. States: Florida led deal activity with 113 transactions followed by California with 110 and Texas with 88, reflecting continued concentration in the nation's largest consumer markets where population growth, tourism demand, and high-density retail and hospitality footprints continue to drive transaction activity.1

Cross-Border Trends: International buyers played a notable role in Q1 2026, highlighted by Switzerland-based Allwyn AG's $2.5 billion acquisition of PrizePicks, Canada-based Boyd Group's $1.3 billion purchase of Joe Hudson's Collision Center, and Israel-based Dan Hotels' acquisition of NoMo SoHo, signaling continued foreign appetite for established U.S. consumer and hospitality platforms.1

| Target | Buyer | Value |

| Off-Highway Business of Dana Incorporated | Allison Transmission Holdings, Inc. | $2,732 |

| Performance Predictions LLC | Allwyn AG | $2,533 |

| JHCC Holdings, LLC | Boyd Group Services Inc. | $1,300 |

| Denny's Corporation | TriArtisan Capital Advisors, LLC; Treville Capital Group LLC; Yadav Enterprises, Inc. | $766 |

| Real estate assets of Bally's Lincoln in Lincoln, Rhode Island | Gaming and Leisure Properties, Inc. |

$700 |

| Topgolf and Toptracer Business of Topgolf Callaway Brands Corp. | Leonard Green & Partners, L.P. | $660 |

| Midwestern Auto Group | Jeff Wyler Automotive Family, Inc. | $500 |

| Inspirato Incorporated | Exclusive Investments, LLC | $239 |

| NoMo SoHo LLC | Dan Hotels Ltd | $121 |

| Nomad Global Communications Solutions, Inc. | Kratos Defense & Security Solutions, Inc. | $1018 |

| Target | Buyer | Value |

| The Houston Grand Hotel | Saddlebrook Equity and Management | $51 |

| Hotel Trio Healdsburg | AWH Partners, LLC | $38 |

| Portland Marriott Downtown Waterfront | Sculptor Capital Management, Inc. | $30 |

| The Last Hotel, at 1501 Washington Ave | Singh Investment Group | $14 |

| 122-room WoodSpring Suites hotel | Noble Investment Group, LLC | $9 |

| Target | Buyer | Value |

| Hilton St. Petersburg Bayfront | Kolter Group Acquisitions LLC | $96 |

| Hilton Garden Inn New York City Tribeca | The Generation Essentials Group | $69 |

| La Posada de Santa Fe Resort & Spa LLC | Crescent Hotels & Resorts, LLC | $57 |

| Walbro LLC | Active Dynamics Group | $50 |

| Hilton Baton Rouge Capitol Center | Northshore Development | $41 |

Source S&P Capital IQ as of 4/1/2026 and PCE Proprietary Data

Opportunities: Improving buyer confidence and PE dry powder deployment should support continued high-conviction transactions, particularly in premium and wellness categories, as companies use M&A to secure critical capabilities and customer access that support long-term growth and resilience.2 3

Risks: Renewed tariff uncertainty in early 2026, inflation sensitivity among lower- and middle-income consumers, and sustained margin pressure in discretionary and mid-tier segments may tighten underwriting standards and elevate execution risk.2

Predicted Activity: Dealmaking will remain selective and precision-oriented, with continued concentration of value into fewer, larger transactions alongside corporate carve-outs and PE take-privates as both strategic and sponsor buyers focus on assets offering resilience and clear paths to value creation.2 3

Joe Anto |

Eric Zaleski |

Kyle Wishing |

Advised Western Milling in their sale to the Western Milling ESOP Trust