Industry Trends

Largest Transactions Closed

- Target

- Buyer

- Value($mm)

Advised Western Milling in their sale to the Western Milling ESOP Trust

Last updated:

Banking, Finance, and Insurance M&A remained steady but selective in Q1 2026. Buyers prioritized strategic fit and resilience over scale for its own sake, with consolidation continuing to drive activity—particularly among banks and insurance platforms. Valuations moved lower as underwriting discipline increased and market uncertainty kept decision-making cautious, elevating the importance of high-quality assets with durable cash flows and clear differentiation (including digital capabilities). Overall, the market signals a shift from volume-driven dealmaking to conviction-led transactions where execution and synergy certainty matter most.1

“Despite moderating deal volume and compressing multiples across FIG, the quality and scale of transactions closing in Q1 underscore a market where conviction is replacing caution," said David Jasmund, Managing Director at PCE. "Bank consolidation has reaccelerated meaningfully, and we expect that momentum to extend into insurance platforms as buyers pursue strategic combinations that strengthen market positioning and operational resilience.”

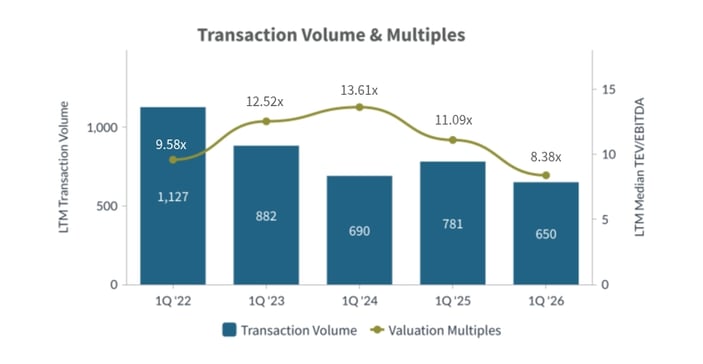

In Q1 2026, Banking, Finance, and Insurance M&A faced continued volume contraction as total deals fell to 650 from 781 a year prior. Both revenue and EBITDA multiples compressed, with TEV/Revenue declining to 1.28x and TEV/EBITDA falling to 8.38x. Premium valuations were concentrated among targets with durable cash flows and differentiated digital capabilities. This dynamic underscores a market where buyers are prioritizing valuation discipline and strategic fit over broad-based expansion amid an uncertain macro backdrop.1

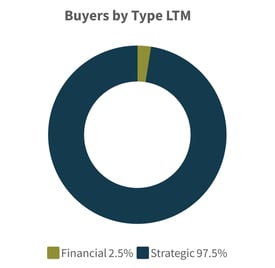

Strategic Acquirers: Strategic buyers continued to command the sector at 97.5% of transactions. Activity centered on regional bank consolidation and insurance platform combinations aimed at building scale and strengthening market positioning in high-growth geographies.1

Financial Buyers: Financial buyers accounted for 2.5% of deal volume, maintaining a selective approach toward high-conviction targets. Sponsor interest remained concentrated in insurance services and specialty advisory businesses where predictable cash flows and operational improvement levers support underwriting at current multiples.1

Global M&A rebounded to its second-highest year on record in 2025, with deal value rising approximately 43% to an estimated $4.7 trillion, while financial institutions M&A climbed 43% to $660 billion. Within this backdrop, Banking, Finance, and Insurance dealmaking accelerated heading into 2026, with U.S. bank M&A on pace in Q1 for its highest quarterly value in seven years as improved regulatory conditions and balance sheet strength encouraged larger, more strategic combinations. 2 4

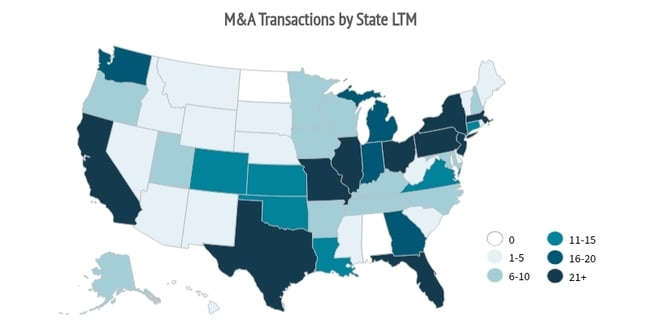

Top U.S. States: Texas led with 54 transactions followed by California with 52 and Florida and New York tied at 36 each, reflecting continued deal concentration in major financial centers and high-growth migration markets.1

Cross-Border Trends: While deal flow remained predominantly domestic, international capital continued to target U.S. financial assets, highlighted by Meiji Yasuda's $2.6 billion restructuring of its North American holdings as Japanese insurers sought to deepen their presence in the U.S. life insurance market.1

| Target | Buyer | Value |

| Comerica Incorporated | Fifth Third Financial Corporation | $10,906 |

| Synovus Financial Corp. | Pinnacle Financial Partners, Inc. | $7,899 |

| Cadence Bank | The Huntington National Bank | $7,592 |

| FirstBank Holding Company | The PNC Financial Services Group, Inc. | $4,079 |

| Meiji Yasuda North America Holdings Incorporated | Meiji Yasuda Life Insurance Company | $2,600 |

| Newfront Insurance Holdings, Inc. | Willis Towers Watson Public Limited Company | $1,450 |

| Cobbs Allen Capital Holdings, LLC | The Baldwin Insurance Group, Inc. | $1,406 |

| MidWestOne Financial Group, Inc | Nicolet Bankshares, Inc. | $866 |

| FineMark Holdings, Inc. | Commerce Bancshares, Inc. | $516 |

| Dogwood State Bank | TowneBank | $491 |

| Target | Buyer | Value |

| Cowell Insurance Services, LLC | Mariner, LLC | n/a |

| Target | Buyer | Value |

| Vista Bancshares, Inc. | National Bank Holdings Corporation | $369 |

| American Bank Holding Corporation | Prosperity Bancshares, Inc. | $328 |

| First Citizens Bancshares, Inc. | Park National Corporation | $317 |

| The Gray Casualty & Surety Company | Palomar Insurance Holdings, Inc. | $300 |

| Middlefield Banc Corp. | Farmers National Banc Corp. | $297 |

Source S&P Capital IQ as of 4/1/2026 and PCE Proprietary Data

Opportunities: Sustained momentum from bank consolidation and PE deployment into insurance platforms should drive elevated deal value, supported by improving financing conditions and a more favorable regulatory environment that give firms greater confidence to pursue strategic transactions.4 5

Risks: Geopolitical trade tensions, tariff-related uncertainty, and macroeconomic volatility remain the primary threats to deal execution, while capital efficiency pressures and heightened focus on investment performance could temper transaction pace in select insurance subsectors.3 5

Predicted Activity: Bank M&A and insurance platform transactions will continue to dominate, with financial services M&A focused on smaller, more strategic capability-driven deals as the sector undergoes structural transformation.2 3

David Jasmund |

Michael Poole |

Kyle Wishing |

Advised Western Milling in their sale to the Western Milling ESOP Trust