Industry Trends

Largest Transactions Closed

- Target

- Buyer

- Value($mm)

Advised Western Milling in their sale to the Western Milling ESOP Trust

Last updated:

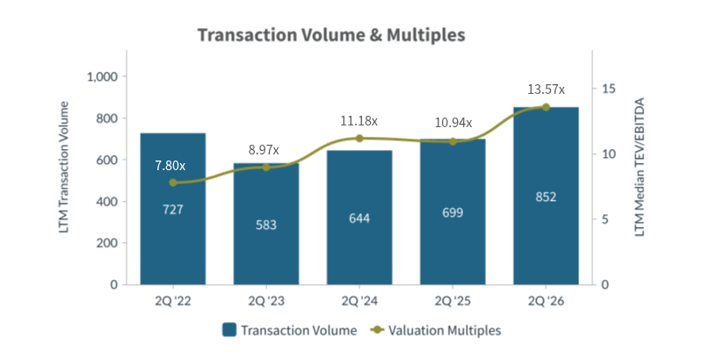

M&A activity in the Building Products and Construction sector accelerated in Q2 2026 with 852 closed transactions (LTM) compared to 699 in the prior year. Strategic buyers dominated by completing 87.5% of deals while financial buyers accounted for 9.8%, remaining selective around fragmented specialty services and infrastructure-oriented platforms. Valuations expanded as median TEV/EBITDA rose to 13.57x from 10.94x and TEV/Revenue strengthened to 2.01x from 1.60x, supported by buyer demand for assets tied to infrastructure, power, data center demand, and durable backlog visibility.

"Building products and construction M&A continued to gain momentum in Q2 as buyers paid up for assets with exposure to infrastructure, power demand, and mission-critical construction," said Nicole Kiriakopoulos, Director at PCE. "The combination of higher deal volume, expanding valuation multiples, and continued strategic buyer activity shows that quality assets are attracting strong interest despite labor and affordability headwinds."

Q2 activity was driven by strategic consolidation in large-scale homebuilding, construction materials, specialty electrical, and infrastructure services, with the largest disclosed transactions concentrated in strategic buyer-led deals. Buyer interest was strongest where targets offered scale, regional density, technical labor, or exposure to infrastructure and power-related demand, while residential-facing assets were underwritten more selectively amid affordability pressure. 1

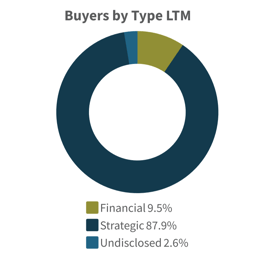

Strategic Acquirers: Strategic buyers continued to lead the sector at 87.5% of transactions, using M&A to add scale, geographic density, and exposure to infrastructure, construction materials, homebuilding, and specialty services markets. Notable activity included Stanley Martin Homes' acquisition of United Homes Group and Breedon Group's acquisition of Casper Stolle Quarry and Contracting Company, reflecting strategic demand for U.S. homebuilding scale and materials expansion.

Financial Buyers: Financial buyers accounted for 9.8% of deal volume, focusing on platform investments and add-ons in fragmented specialty contracting, infrastructure services, engineering, permitting, and maintenance-oriented subsectors. Sponsor activity remained disciplined, with capital directed toward businesses offering recurring demand, regional expansion potential, and clear buy-and-build opportunities.1

Building Products and Construction dealmaking strengthened through Q2 2026 as capital concentrated around assets tied to infrastructure demand, construction services, and resilient specialty platforms. While labor constraints and residential affordability continued to weigh on portions of the market, buyers remained active where targets offered technical capabilities, durable backlogs, and exposure to mission-critical construction demand.2 3 4 5

Building Products and Construction dealmaking strengthened through Q2 2026 as capital concentrated around assets tied to infrastructure demand, construction services, and resilient specialty platforms. While labor constraints and residential affordability continued to weigh on portions of the market, buyers remained active where targets offered technical capabilities, durable backlogs, and exposure to mission-critical construction demand.2 3 4 5

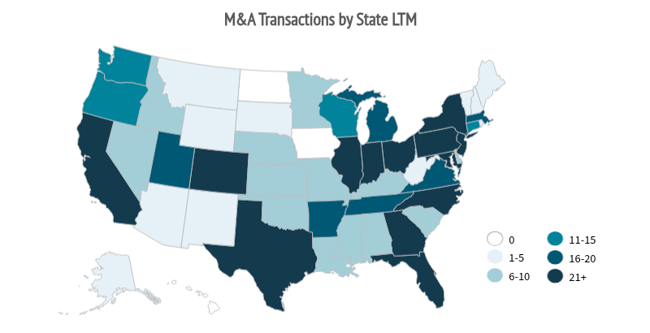

Top U.S. States: Texas, Florida, and California remained the most active states, supported by infrastructure, construction services, and specialty trade activity; in Florida, continued transaction volume should be viewed alongside a softer new-home construction backdrop, where builders remain active in select markets despite broader residential pressure.1 5

Cross-Border Trends: Deal flow in Q2 2026 remained primarily domestic, though select cross-border acquirers were active, including Breedon Group's acquisition of Casper Stolle Quarry and Contracting Company and Hexatronic Group's acquisition of Superior Fiber & Data Services. Overall activity continued to center on U.S.-based assets tied to infrastructure, construction materials, and specialty services.1

| Target | Buyer | Value ($mm) |

| Tri Pointe Homes, Inc. | Sumitomo Forestry America Inc. | $5,400 |

| American Woodmark Corporation | MasterBrand, Inc. | $1,383 |

| Great Lakes Dredge & Dock Company, LLC | Saltchuk Resources, Inc. | $1,372 |

| Ready-Mixed Concrete Business Assets of Vulcan Materials Company | CalPortland Company | $712 |

| PayneCrest Electric, Inc. | Primoris Services Corporation | $400 |

| Keystone Cement Company, LLC | Titan America SA | $310 |

| United Homes Group, Inc. | Stanley Martin Homes, LLC | $218 |

| Casper Stolle Quarry And Contracting Company | Breedon Group plc | $120 |

| Nelson Bros. Ready Mix, LLC | Hope Concrete Company | $80 |

| I-4 Mobility Partners Opco LLC | John Laing Group Limited | $75 |

| Target | Buyer | Value ($mm) |

| Blast All Inc | OEP Capital Advisors L.P. | n/a |

| Cumming Management Group, Inc. | Leonard Green & Partners, L.P. | n/a |

| Main Line Commercial Pools, Inc. | Warren Equity Partners, LLC | n/a |

| Milrose Consultants, LLC | Littlejohn & Co., LLC | n/a |

| ADF Engineering LLC | Heartland Growth Partners, LLC | n/a |

| Target | Buyer | Value ($mm) |

| Motiv Space Systems, Inc. | Rocket Lab Corporation | $60 |

| Hope Concrete Company | Concrete Partners, LLC | $44 |

| Newoods, Inc. | Suncrete, Inc. | $37 |

| Superior Fiber & Data Services, Inc. | Hexatronic Group AB | $29 |

| EnergyAid, Inc. | Otovo Inc. | $12 |

Source S&P Capital IQ as of 7/1/2026 and PCE Proprietary Data

Opportunities: Demand from data centers, power infrastructure, grid modernization, water systems, and public infrastructure should continue to support M&A for targets with technical capabilities, durable backlogs, and exposure to mission-critical construction spend.2 3 4

Risks: Elevated construction input prices, skilled labor scarcity, and weak residential affordability could pressure margins and slow activity for targets without pricing power, backlog visibility, or exposure to stronger infrastructure-oriented demand.4 5

Predicted Activity: Near-term deal activity is expected to remain selective but active, with buyers prioritizing scaled platforms and add-ons that offer regional density, technical capabilities, and exposure to infrastructure-related demand. Larger strategic transactions suggest continued interest in assets with defensible market positions and clear integration or expansion potential.1 2 3 4

Nicole Kiriakopoulos |

Michael Poole |

Will Stewart |

Advised Western Milling in their sale to the Western Milling ESOP Trust