Industry Trends

Largest Transactions Closed

- Target

- Buyer

- Value($mm)

Last updated:

Key takeaways:

If you are an early-stage company looking to raise capital from a venture capital or private equity firm, you have likely heard of preferred stock. But are you familiar with all their rights and features? Similar to common stock, preferred stock offers equity ownership in a company. Shareholders of preferred stock, however, have priority on dividends and earnings and have seniority on liquidation preferences.

Preferred stock not only has priority over common stock but depending upon the terms negotiated, preferred stock can convert or participate with common stock. These conversion and participation features could have a significant impact on the proceeds available to common stockholders.

This article will help you understand how preferred stock liquidation preferences, dividends, conversion features and participation rights impact your payout in a liquidation event.

Liquidation preferences determine the order in which proceeds will be distributed to various equity classes upon a liquidity event. Preferred shareholders usually receive proceeds before common shareholders upon such event. Liquidity events can be anything ranging from dissolution to an IPO, sale, or merger of a company.

Preferred shareholders receive proceeds before common shareholders upon a liquidity event, and at a minimum, those proceeds are typically equal to the initial contribution. Depending on how liquidation preferences are structured, preferred shareholders could receive significantly more than their initial contribution.

Calculations follow standard payout conventions and reflect common variations in preference structures to ensure clarity in valuation outcomes.

Preferred stock commonly has features similar to debt in that preferred shareholders receive dividends on their investment. Dividends can be paid out quarterly or annually, or they can accrue and even compound.

Conversion features specify the exchange rate between preferred and common shares and determine whether preferred holders will convert to maximize returns based on company value and anti-dilution adjustments.

Depending on your company’s success, preferred shareholders may find it more beneficial to convert to common stock and participate in the proceeds as common shareholders. The rate at which preferred stock converts to common stock is normally agreed upon at the time of investment and is outlined in the preferred stock agreement or similar legal documents. The conversion rate is based on the terms negotiated, and is not always one-to-one. Preferred shareholders could achieve a significant return by converting to a much higher number of common shares. The conversion ratio may even be adjusted from time to time to prevent dilution of ownership due to subsequent financing rounds.

Apply fair value measurement principles when determining how convertible instruments and conversion features should be recognized in financial statements.

Conversion terms are defined in transaction documents and are analyzed using established valuation methods to determine when conversion yields a greater economic return.

Participation rights define whether preferred shareholders share in upside after receiving their liquidation preference and whether that participation is unlimited, capped, or absent, with direct implications for common shareholder dilution.

The level of participation by preferred shareholders can typically be categorized as follows:

Below are a few examples illustrating how proceeds from a liquidity event are distributed to various equity classes. The case studies present hypothetical capital structures and three payout scenarios—full participation, capped participation, and non-participation—to illustrate how preferred terms change proceeds allocation across company values.

Startup, Inc. raised $10.0 million in a Series A financing round from a private equity firm. The hypothetical capital structure and features of the preferred are as follows:

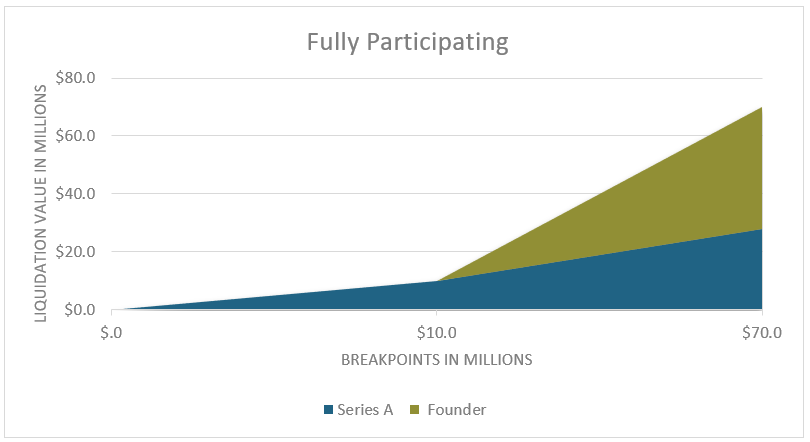

In this scenario, the Series A investor receives its preliminary liquidation preference of $10.0 million. Since the company sold for $70.0 million and the Series A is a participating preferred instrument in this scenario, Series A would participate pro rata with the founder in the additional proceeds and receive another 30.0% of the amount above the $10.0 million liquidation preference, or $18.0 million. The total proceeds received by the Series A investor would equal $28.0 million or 40.0% of the total proceeds, which is much greater than the 30.0% ownership interest. The chart below illustrates how each class participates based on the value of the company.

As illustrated above, the lower the value of the company, the more Series A receives as a percent of the total. To decrease the dilutive impact of a participating preferred investor, a non-participating or capped participation feature would be suggested.

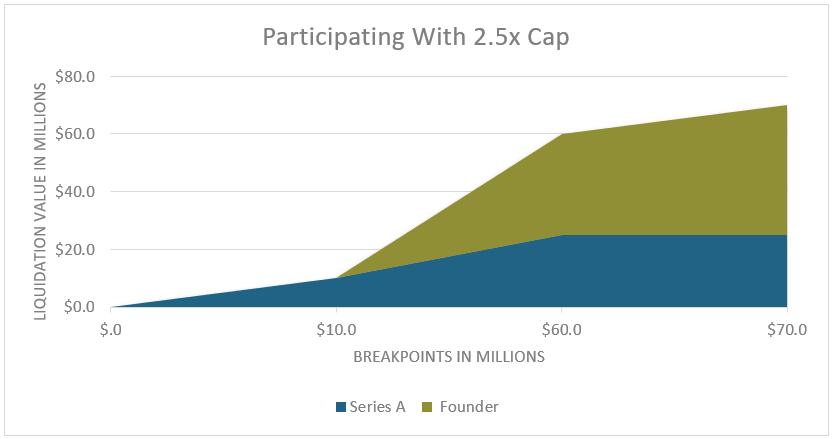

In scenario 2, the Series A investor receives its initial contribution or liquidation preference of $10.0 million. Proceeds above $10.0 million are then shared pro rata between the Series A investor and the founder until Series A receives its maximum benefit of $25.0 million (2.5x the original investment). The remaining amount ($10.0 million) is then allocated 100.0% to the founder. In this scenario, the Series A investor receives 35.7% of the total proceeds, compared to the 40.0% received in scenario 1. The chart below illustrates how the proceeds received by the founder increase substantially once the Series A investor achieves the 2.5x threshold.

As illustrated in this graph, Series A reaches a plateau once the $25.0 million threshold is achieved. What is not illustrated, however, is what happens in scenarios where the company sells for a higher price, and it would be more beneficial for the Series A investor to forgo their rights as a preferred investor and convert to common. To estimate this threshold, we would want to know at what company value the Series A investor would convert in order for it to achieve a greater benefit. Understanding typical valuation fees helps firms budget for the financial analysis required to estimate conversion thresholds.

In this scenario, given that Series A stops receiving benefit at $25.0 million, they would want to convert once their pro rata interest as a common shareholder is greater than $25.0 million. The answer is to simply divide the $25.0 million threshold by their pro rata portion of the equity, which in these examples is 30.0%. Accordingly, the Series A investor would likely convert to common at any value greater than $83.3 million ($25.0 million / 30.0% = $83.3 million).

While the dilution to the founder or common shareholder is not as significant as that in scenario 1, issuing preferred shares with even a capped participation feature can greatly reduce the proceeds to common shareholders. Issuing preferred shares with no participation feature is one way to help reduce dilution as outlined in the following scenario.

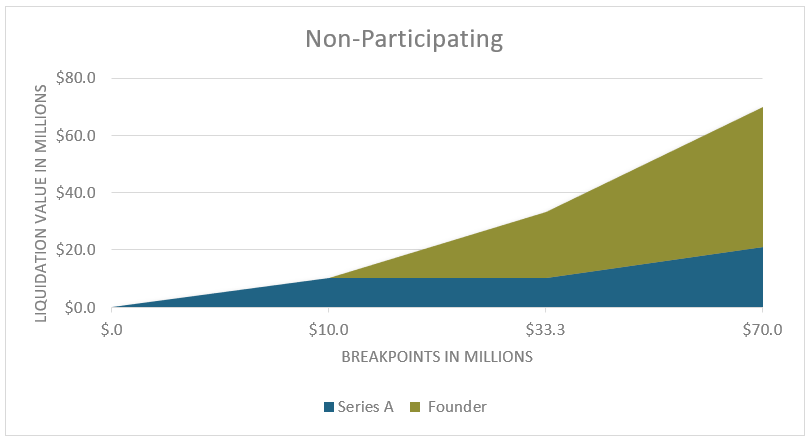

In scenario 3, Series A receives a liquidation preference equal to their original investment of $10.0 million and then no longer receives any proceeds, since it is a non-participating preferred security. Proceeds above the $10.0 million liquidation preference are then distributed 100.0% to the founder. Given Series A has the ability to convert to common stock, however, the Series A investor would exercise their right to convert when proceeds from a liquidity event exceed their $10.0 million preference. Similar to the conversion calculation we performed in scenario 2, the Series A investor would convert to common stock at a company value of $33.3 million ($10.0 million / 30.0% = $33.3 million). At any liquidation value above this threshold, the Series A investor would now be a common shareholder and receive 30.0% of all proceeds, maximizing their return. The following chart illustrates how proceeds are allocated based on company values.

This chart illustrates how the Series A investor receives the same payout if Startup, Inc. liquidates for $10.0 million or $33.3 million, but then receives increased proceeds once the value of the company exceeds $33.3 million.

The examples use hypothetical figures with transparent assumptions to demonstrate how alternate preferred terms change distribution outcomes across a range of company values.

Comparing the scenarios shows that non-participating preferred with no conversion or participation features typically maximizes common shareholder returns, while full participation materially reduces common upside.

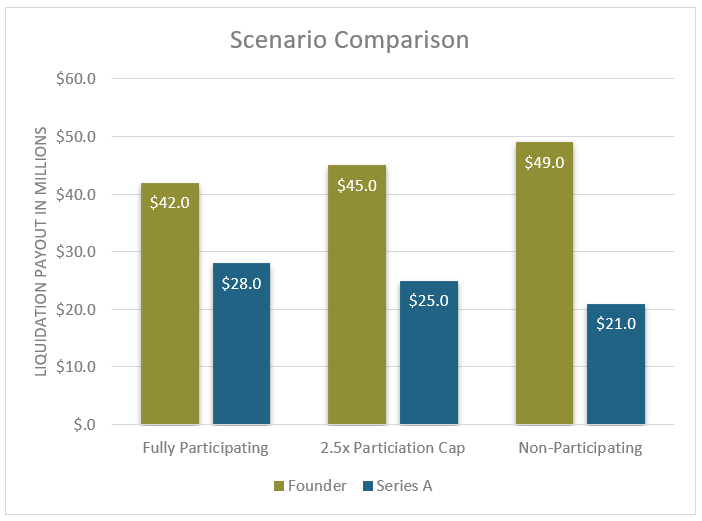

The following chart compares the proceeds resulting from the three scenarios:

It is not surprising to see that when preferred investors do not participate with common stock, the total return to the common shareholders is maximized and, in our example, the founder’s distribution totaled $49.0 million. Preferred stock that fully participates results in the least amount distributed to common shareholders. Valuation techniques such as the multi-period excess earnings method can help quantify how participation features affect equity distributions. In our examples, the preferred investor did not receive any dividends, which is uncommon. Had the preferred investor received dividends, the proceeds received by the common shareholders would have been reduced even further under all scenarios.

Even when preferred stock does not participate as common stock, but has the ability to convert to common stock, the common shareholders are still forgoing their full potential. In order to fully mitigate any dilution, you would be best served to issue preferred stock with no participation or conversion features. This type of preferred instrument would be similar to that of a debt instrument in that once liquidation is achieved, only the initial investment and dividends are paid to the preferred investors, allowing the common shareholders to benefit from all the upside.

Conclusions are grounded in standard valuation principles and observable term-sheet variations to highlight how specific preferred provisions affect common shareholder outcomes.

Q: What is a liquidation preference and how does it affect payout?

A: A liquidation preference gives preferred shareholders priority to proceeds from a liquidity event, typically guaranteeing at least the return of the original investment before common shareholders receive distributions. Depending on its structure, the preference can also entitle preferred holders to additional proceeds, which reduces what remains for common shareholders.

Q: How do participation rights change what preferred shareholders receive?

A: Participation rights determine whether preferred shareholders share in remaining proceeds after receiving their liquidation preference. Full participation allows preferred holders to take both their preference and a pro rata share of upside, capped participation limits total return to a specified multiple before common receives remaining proceeds, and non-participating preferred receive only their preference unless converting to common yields a higher return.

Q: When would preferred shareholders convert to common stock?

A: Preferred shareholders convert when the economic return as common shareholders exceeds their liquidation preference, based on the agreed conversion ratio and ownership percentages. Conversion thresholds are calculated by comparing the as-converted pro rata share to the capped or uncapped preference to determine which yields a greater payout.

Q: What is a participation cap and how is a cap like 2.5x applied?

A: A participation cap limits the total proceeds a participating preferred investor can receive to a predefined multiple of the original investment, such as 2.5x. The preferred holder receives their liquidation preference and shares pro rata in upside until the cap is reached, after which remaining proceeds are allocated to common shareholders.

Q: How do dividends on preferred stock affect common shareholder proceeds?

A: Dividends paid or accrued to preferred shareholders reduce the pool of proceeds available to common shareholders, since dividends are typically paid before common distributions. If dividends compound or accrue, the impact on common proceeds increases, further reducing common shareholder returns under the same liquidity outcome.

Paul Vogt

Paul Vogt is a Managing Director at PCE and leads the firm’s valuation practice from its Atlanta office. With over 20 years of experience, he specializes in business valuations for financial reporting, tax planning, litigation support, and corporate strategy across a wide range of industries.

Valuation

pvogt@pcecompanies.com

Atlanta Office

407-621-2100 (main)

678-641-4760 (direct)

407-621-2199 (fax)