Industry Trends

Largest Transactions Closed

- Target

- Buyer

- Value($mm)

Last updated:

Key takeaways:

In today’s economy, intangible assets are often the most valuable part of a company, especially in service-based and technology-driven businesses. These non-physical assets, like intellectual property and brand reputation, can account for more than half of a company’s total enterprise value.

Yet many business owners ask:

“How do I value my intangible assets?”

Let’s start with what we mean by intangible assets.

Intangible assets encompass non-physical resources such as intellectual property, brand reputation, customer relationships, marketing-related assets, business processes, software, and creative works, and these assets often drive a substantial portion of enterprise value.

These assets are not found on the factory floor - but they’re central to business value.

MPEEM is most appropriate when a clearly identifiable primary intangible asset generates measurable excess earnings and when valuation is needed for strategic planning, fundraising, M&A purchase price allocations, financial reporting, or competitive analysis.

MPEEM is most appropriate when a clearly identifiable primary intangible asset generates measurable excess earnings and when valuation is needed for strategic planning, fundraising, M&A purchase price allocations, financial reporting, or competitive analysis.

The Multi-Period Excess Earnings Method (MPEEM) is a commonly used income-based valuation method for intangible assets.

MPEEM is particularly relevant during:

In essence, you're valuing what’s left, the “excess” earnings generated by your key intangible asset.

The MPEEM is widely applied in ASC 805 purchase price allocations and financial reporting engagements, and its use is supported by established valuation practice when contributory asset charges and assumptions are thoroughly documented.

Understanding the MPEEM and other methods for valuing intangible assets is important for a few reasons. Here’s when this approach becomes essential:

Strategic Planning: Understanding the value of your company’s intangible assets can help you make strategic decisions, such as deciding whether to enter a particular market or how to price products.

Fundraising: When raising capital, you might need not only to prove your business’s value to investors, but also to show your intangible assets’ value to persuade them to invest. Whether those intangible assets are internally created or gained through acquisitions, understanding how to value them and prove to investors that they can create profits is crucial when trying to raise the capital you need.

Mergers and Acquisitions (M&A): Understanding how to value intangible assets can help you negotiate a fair price in an M&A transaction. Following your acquisition of another company, that understanding can help you assess and capitalize the assets obtained.

Accounting and Reporting: Because you must report the fair value of intangible assets on financial statements, understanding the MPEEM, as well as other valuation methods, can help you determine the proper values to report.

Competitive Analysis: Understanding the value of competitors’ intangible assets can help you understand their market position and identify opportunities for differentiation.

The upshot is that understanding the MPEEM and how this method compares with other methods for valuing intangible assets can help you make informed decisions about your business’s management and growth.

The first step in using the MPEEM to value your company’s primary intangible asset is identifying the asset and its potential uses. As part of this step, you will want to consider expectations and estimate future cash flows the asset will likely generate. This process typically involves assuming the market size for the asset, the asset’s penetration rate in that market, and the expected margin on sales of the asset.

asset and its potential uses. As part of this step, you will want to consider expectations and estimate future cash flows the asset will likely generate. This process typically involves assuming the market size for the asset, the asset’s penetration rate in that market, and the expected margin on sales of the asset.

Today's Capital Markets provides context on market factors that can influence expected cash flows and valuation assumptions.

Once you estimate the future cash flows, you can use a discounted cash flow (DCF) model to estimate those cash flows’ present values. The discount rate used in the DCF model should reflect the risk of that asset’s cash flows and be consistent with the risk of other investments with similar features.

When using the MPEEM to value your company’s primary intangible asset, remember some important things. One is that the method relies heavily on assumptions about future cash flows and market conditions, which can be difficult to predict. Another is that the method might not account for all the asset’s possible uses, so the value estimate might be low.

Finally, like other valuation methods, the MPEEM will be more accurate when combined with other methods and after critical analysis. Intangible asset valuation is not an exact science, and you must be transparent about the assumptions and methodologies used when presenting the value estimate.

Things to Consider in a Preferred Stock Capital Raise highlights valuation and structuring factors relevant when using intangibles in fundraising.

Documenting core assumptions and conducting sensitivity testing are standard practice when presenting MPEEM results to stakeholders and auditors to ensure the valuation withstands technical review.

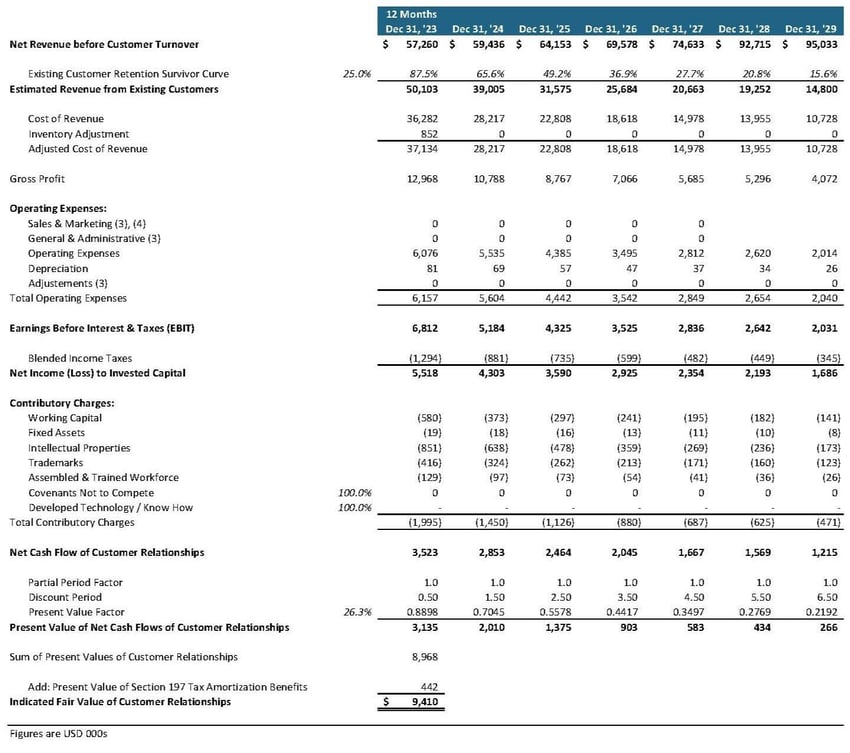

A valuation professional held detailed discussions with the management of Company X, the target of an acquisition, to identify Company X’s tangible and intangible assets. Based on these discussions, these assets were identified: net working capital, fixed assets, customer relationships, intellectual properties, trademarks, and assembled workforce. These discussions determined that customer relationships were Company X’s primary asset.

The following reflects the valuation analysis of Company X’s customer relationships:

Observations:

Observations:Q: What is the Multi-Period Excess Earnings Method (MPEEM)?

A: The MPEEM is an income-based valuation method that isolates the excess cash flows attributable to a company's primary intangible asset after applying contributory charges for supporting assets, and then discounts those excess earnings to present value to estimate the asset's fair value.

Q: When is it appropriate to use the MPEEM?

A: MPEEM is appropriate when a primary intangible asset generates identifiable excess earnings and valuation is needed for strategic planning, fundraising, M&A purchase price allocations, financial reporting, or competitive analysis; the method is particularly useful in contexts governed by ASC 805 and similar reporting requirements.

Q: Which types of intangible assets are commonly valued with MPEEM?

A: Common candidates include customer relationships and databases, intellectual property, brand and trademark value, marketing-related intangibles, business processes, and software, with the method best suited to assets that drive measurable future cash flows.

Q: What are the main steps in applying the MPEEM?

A: Core steps include identifying the primary intangible asset and its uses, estimating the asset's future cash flows and market penetration, applying contributory charges for supporting assets, discounting excess earnings with an appropriate risk-adjusted rate, and documenting assumptions and sensitivity testing to support the valuation.

Q: Why should a valuation professional be engaged for an MPEEM analysis?

A: MPEEM requires technical adjustments, judgment about contributory charges and attrition, and alignment with accounting and tax rules; a qualified valuation professional provides the expertise to develop defensible assumptions, prepare thorough documentation, and address regulatory and reporting requirements.

Valuing intangible assets with MPEEM requires careful judgment, transparent documentation of assumptions, and technical adjustments tied to accounting and tax rules, which typically necessitates qualified valuation expertise to produce defensible conclusions.

As this article demonstrates, using the MPEEM to value an intangible asset can be complex. Further, a purchase price allocation that uses the MPEEM to determine a particular intangible asset’s value adds complexities. As illustrated above, there are several factors and assumptions must be considered when using the MPEEM.

Fair Value Measurement for Financial Reporting describes valuation techniques and the fair value hierarchy useful when performing purchase price allocations.

When selecting which methodologies to use to value individual intangible assets, consider the facts and circumstances unique to your company and its assets. Much research, thought, and experience are required when using the MPEEM, especially when performing a purchase price allocation. If you are considering how to value your intangible assets or need to perform a purchase price allocation, we highly recommend hiring a qualified valuation analyst — the benefits of doing so far outweigh the costs.

The Cost of a Valuation outlines typical cost drivers and engagement considerations when hiring valuation professionals.

Engagements that involve purchase price allocations, ASC 805 compliance, or tax amortization considerations commonly require specialized valuation expertise to develop defensible conclusions and documentation.

Paul Vogt

Paul Vogt is a Managing Director at PCE and leads the firm’s valuation practice from its Atlanta office. With over 20 years of experience, he specializes in business valuations for financial reporting, tax planning, litigation support, and corporate strategy across a wide range of industries.