Industry Trends

Largest Transactions Closed

- Target

- Buyer

- Value($mm)

Advised Western Milling in their sale to the Western Milling ESOP Trust

Last updated:

Food & Agriculture M&A moderated in Q1 2026 as buyers stayed selective amid macro uncertainty and tighter underwriting. Strategic acquirers remained the primary source of demand, while financial sponsors modestly increased participation.

According to Michael Poole, Managing Director at PCE, “The Food & Agriculture M&A market has shifted from a volume story to a quality story—buyers are concentrating capital on assets with defensible positions, resilient earnings, and strong supply chains, even amid macro headwinds.”

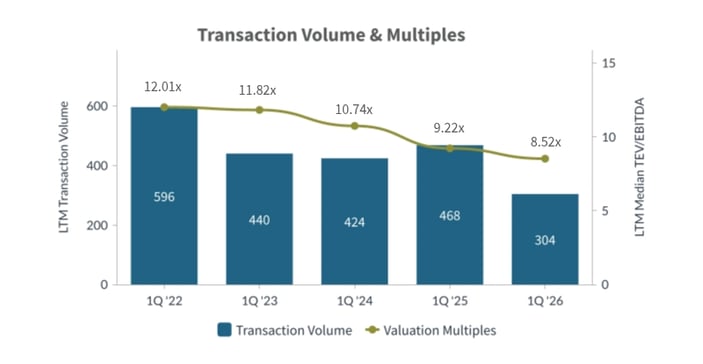

Valuations remained under pressure (median TEV/EBITDA of 8.52x and TEV/Revenue of 1.34x), reinforcing the market’s shift toward earnings quality and resilient supply chains.

Valuation compression continued into Q1 2026, with median TEV/EBITDA declining to 8.52x from 9.22x in Q1 2025 LTM — the fourth consecutive year of multiple contraction from the 12.01x peak in Q1 2022. Revenue multiples held roughly flat at 1.34x, consistent with the prior year, suggesting buyers remain willing to underwrite top-line scale but are demanding stronger earnings profiles. Deal flow of 304 LTM transactions reflects a 35% decline from the Q1 2025 LTM level, underscoring a market where strategic discipline and selective deployment have replaced volume-driven activity.

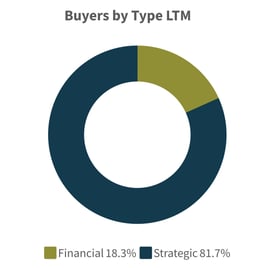

Strategic Acquirers: Strategic buyers represented 81% of transactions (247 of 304 LTM), concentrating on branded food platforms, protein, beverage, and specialty agricultural assets. Notable transactions include Premium Brands Holdings’ $775.84M deal for Stampede Culinary Partners and Anheuser-Busch’s $490M acquisition of Future Proof Brands.

Financial Buyers: Financial buyers accounted for 19% of deals (57 of 304 LTM), an increase from 13% in Q1 2025, with activity centered on value-added food platforms and niche specialty categories. Firms including Highlander Partners, PPC Investment Partners, and Humble Management targeted businesses with strong operational upside and defensible market positions.

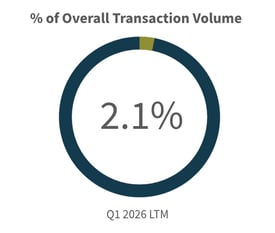

In Q1 2026, Food & Agriculture M&A activity decelerated relative to the prior year, with 304 LTM closed transactions representing approximately 2.1% of overall market volume (14,429 LTM deals), down from a higher share in prior periods. The sector accounted for 1.8% of Q1 2026 standalone deal flow (64 of 3,515 total closed transactions), reflecting consolidation pressure amid compressed valuations, tariff-driven input cost uncertainty, and tighter credit conditions. Despite the volume decline, large-scale strategic deals — including three transactions above $500M in Q1 2026 alone — signal that high-quality assets with defensible market positions continue to attract significant buyer interest.

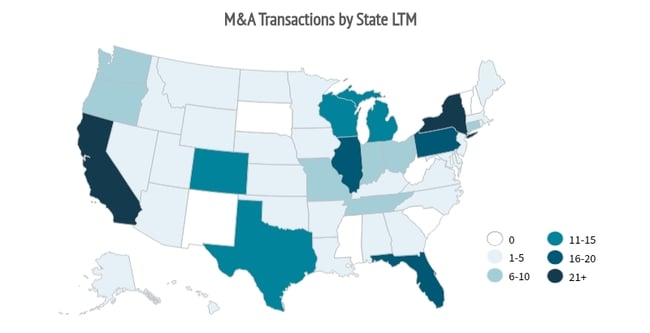

Top U.S. States: California led deal activity with 54 transactions, followed by New York (23), Illinois (17), Pennsylvania (16), and Texas (14), reflecting continued concentration in major food processing, distribution, and innovation corridors.

Cross-Border Trends: Foreign buyers remained active, with transactions such as Agrolimen SA’s $600M acquisition of Ollie Pets and Cobram Estate’s $173.5M deal for California Olive Ranch highlighting sustained international appetite for U.S. food and agriculture assets. However, escalating tariff uncertainty and trade policy volatility may temper cross-border activity heading into Q2 2026.

| Target | Buyer | Value |

| TreeHouse Foods, Inc. | InvestIndustrial | $3,018 |

| Stampede Culinary Partners, Inc. | Premium Brands Holdings Corporation | $776 |

| Ollie Pets Inc. | Agrolimen SA | $600 |

| Future Proof Brands LLC | Anheuser-Busch Companies, LLC | $490 |

| California Olive Ranch, Inc. | Cobram Estate Olives Limited | $174 |

| Creighton Brothers, LLC | Cal-Maine Foods, Inc. | $130 |

| Navitas LLC | Laird Superfood, Inc. | $39 |

| University Rx Specialists, Inc. | Fagron NV | $30 |

| Target | Buyer | Value |

| Nacho Eats Corp. | Natpets, LLC | n/a |

| VelociGro Inc. | Klasmann-Deilmann GmbH | n/a |

| Primal Pet Foods, Inc. | Pure Treats Inc. | n/a |

| Chiyo, Inc. | Epicured Meal Delivery, LLC | n/a |

| Arctic Glacier U.S.A., Inc. | Reddy Ice LLC | n/a |

| Target | Buyer | Value |

| Smith Gardens, Inc. | Hoffmann Family of Companies | n/a |

| SimplyFUEL LLC | Humble Management, LLC | n/a |

| Tapatio Foods, LLC | Highlander Partners, L.P.; The Arnold Companies | n/a |

| NaturPak | PPC Investment Partners LP | n/a |

Source S&P Capital IQ as of 4/2/2026 and PCE Proprietary Data

Opportunities: Buyers are paying up for high-growth brands, and the IPO window is reopening (e.g., Once Upon A Farm’s $198M IPO at ~4x revenue and Suja’s expected listing). 7

Risks: “Liberation day” tariffs are expected to flow through to consumer prices between April and October 2026, pressuring margins and promotional funding as weak sentiment and high rates limit spending outside top-income cohorts. 4

Predicted Activity: Expect continued unbundling among diversified agribusiness platforms and faster within-segment consolidation, with middle-market food manufacturing and branded CPG deals rising as subscale brands face retailer pressure and scaled strategics. 7

David Jasmund |

Michael Poole |

Will Stewart |

Advised Western Milling in their sale to the Western Milling ESOP Trust