Industry Trends

Largest Transactions Closed

- Target

- Buyer

- Value($mm)

Advised Western Milling in their sale to the Western Milling ESOP Trust

Last updated:

Healthcare M&A activity showed improvement in Q2 2026, with deal volume stabilizing as buyer confidence gradually returned. Strategic acquirers continued to lead activity, focusing on diagnostics, life sciences, and tech-enabled care, while financial sponsors selectively pursued scalable platforms in niche segments.2

“Healthcare M&A activity in Q2 reflects a measured reengagement of buyers as market clarity improves,” said Brad Scharfenberg, Vice President at PCE. “Transactions are increasingly concentrated in high-quality platforms with scalable growth, resilient margins, and strong strategic alignment.”

Valuation multiples remained disciplined but showed early signs of improvements, with continued emphasis on durable growth and defensible business models. Below, we highlight key transactions, geographic trends, and emerging themes shaping the Healthcare M&A landscape.2

Ongoing macroeconomic uncertainty and a cautious financing environment continued to influence Healthcare M&A in Q2 2026, though transaction volume showed stabilization relative to Q1 levels. Valuation multiples showed signs of improvement, as median TEV/Revenue increased to 3.5x—up from 3.2x in the prior year. EBITDA multiples also increased to 14.0x—significantly up from 12.0x a year ago. Buyers continued to prioritize assets with cost efficiency, reimbursement stability, and exposure to outpatient and home-based care—segments viewed as lower-risk within the evolving healthcare delivery landscape.3

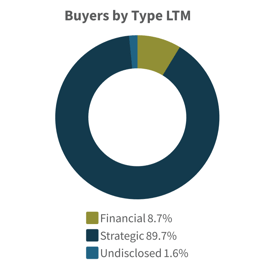

Strategic Acquirers: Strategic acquirers continued to lead Healthcare M&A activity in Q2 2026, focusing on capability expansion in high-growth therapeutic areas. Notably, Arlo Technologies’ acquisition of Perfuse Therapeutics for $2.5B highlights continued appetite for large-scale, pipeline-driven transactions, particularly as strategic buyers seek to diversify into adjacent biomedical platforms, offset near-term revenue concentration, and strengthen long-term growth through differentiated therapeutic assets. Strategic dealmaking remained concentrated in life sciences, diagnostics, and biopharma, with an emphasis on differentiated assets and late-stage pipelines.4

Financial Buyers: Financial sponsors remained selective in Q2 2026, maintaining a disciplined approach focused on platform scalability, recurring revenue, and operational efficiency. Private equity activity continued to center on mid-market add-ons and platform investments, particularly in healthcare services and technology-enabled care sectors, where sponsors can drive value through consolidation and operational improvement. This targeted deployment of capital reflects ongoing selectivity and a preference for defensible business models with clear cash flow visibility.4

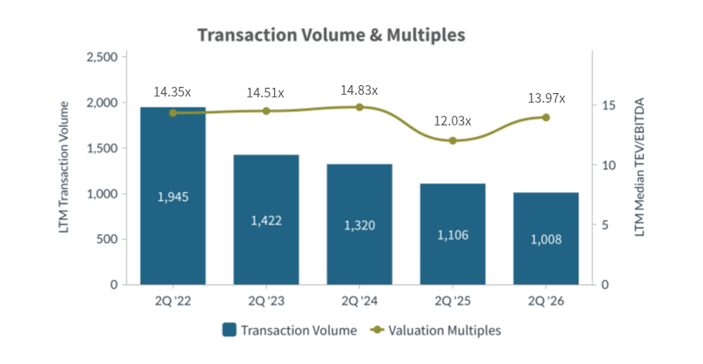

Healthcare M&A volume remained below prior-year levels on an LTM basis through Q2 2026, though activity showed early signs of stabilization relative to Q1. The sector continues to outperform more cyclical industries in deal resilience, accounting for a meaningful share of total M&A activity, supported by its non-discretionary demand profile and long-term demographic tailwinds. Valuation multiples expanded, with TEV/EBITDA increasing to 14.0x and TEV/Revenue reaching 3.5x; however, buyers maintained disciplined underwriting standards despite sustained capital interest in the sector.

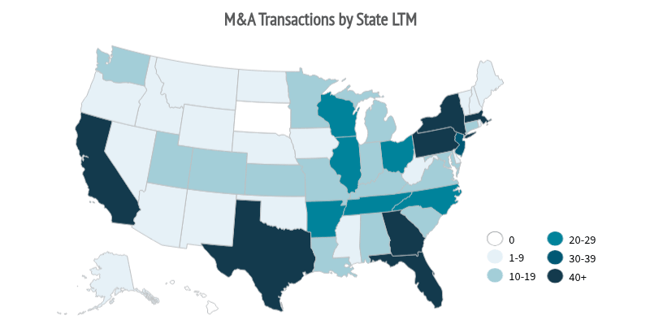

Top U.S. States: California (146 deals), Florida (89), and Texas (67) remained the most active Healthcare M&A markets on a trailing basis through Q2 2026, supported by strong provider networks, favorable demographics, and concentrated innovation hubs. Massachusetts (60) and New York (54) also remained highly active, reflecting continued consolidation in large healthcare markets.

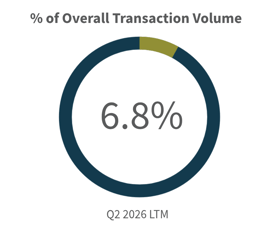

Cross-Border Trends: Cross-border activity remained active in Q2 2026, with international buyers continuing to target U.S. healthcare assets to access innovation and pipeline development. Notably, Servier (France) completed its acquisition of Day One Biopharmaceuticals (U.S.) for approximately $2.5B, underscoring sustained foreign interest in U.S. oncology pipelines and the strategic appeal of commercially ready pediatric cancer assets as a platform for international expansion.

| Target | Buyer | Value ($mm) |

| Hologic, Inc. | Blackstone Inc.; GIC Private Limited; Abu Dhabi Investment Authority; TPG Global, LLC | $20,582 |

| Masimo Corporation | Danaher Corporation | $10,135 |

| Arcellx, Inc. | Gilead Sciences, Inc. | $7,593 |

| Terns Pharmaceuticals, Inc. | Merck Sharp & Dohme LLC | $6,865 |

| Apellis Pharmaceuticals, Inc. | Biogen Inc. | $6,763 |

| Amicus Therapeutics, Inc. | BioMarin Pharmaceutical Inc. | $5,231 |

| Select Medical Holdings Corporation | Welsh, Carson, Anderson & Stowe, L.P. | $4,979 |

| AMSURG Corp. | Ascension Health Alliance | $3,900 |

| Soleno Therapeutics, Inc. | Neurocrine Biosciences, Inc. | $2,647 |

| Day One Biopharmaceuticals, Inc. | Servier Pharmaceuticals LLC | $2,510 |

| Target | Buyer | Value ($mm) |

| Celerion Holdings, Inc. | Thomas H. Lee Partners, L.P. | $1,800 |

| Enhabit, Inc. | Kinderhook Industries, LLC | $1,281 |

| The Aston Gardens at Parkland Commons Senior Living Facility in Broward County | Ventas, Inc. | $64 |

| Cohero | Arcadea Group Inc. | n/a |

| TC Manufacturing Inc. | Teleo Capital Management LLC | n/a |

| Target | Buyer | Value ($mm) |

| Global rights to RADICAVA ORS and IV RADICAVA from Tanabe Pharma Provision Co., Ltd | Shionogi Inc. | $2,500 |

| Perfuse Therapeutics, Inc. | Bayer Aktiengesellschaft | $2,450 |

| Ajax Therapeutics, Inc. | Eli Lilly and Company | $2,300 |

| Candid Therapeutics, Inc. | UCB SA | $2,200 |

| Ouro Medicines, Inc. | Gilead Sciences, Inc. | $2,175 |

Source S&P Capital IQ as of 7/1/2026 and PCE Proprietary Data

Opportunities: Improving market visibility and selective reengagement from both strategic and financial buyers are supporting a gradual pickup in healthcare M&A activity in Q2 2026. Investors continue to target high-quality assets in technology-enabled care, life sciences, and outpatient services, with capital increasingly flowing toward scalable platforms with strong margins and clear growth pathways.2

Risks: Macroeconomic uncertainty, reimbursement visibility, and regulatory oversight remain key headwinds in Q2 2026, continuing to influence deal pacing and valuation discipline. Ongoing policy changes and cost pressures across providers and payors are contributing to a more selective investment environment, with buyers remaining cautious on assets exposed to regulatory or reimbursement volatility.2

Predicted Activity: Healthcare M&A in Q2 2026 continues to be defined by precision over volume, with buyers prioritizing differentiated assets that offer durable cash flows, scalable operating models, and strong strategic alignment. Dealmaking remains focused on targeted acquisitions—particularly in AI-enabled platforms, specialty care, and biopharma pipelines—while underwriting standards emphasize execution risk, integration planning, and long-term value creation over headline valuation metrics.2

David Jasmund |

Jon Gogolak |

Bradley Scharfenberg |

Advised Western Milling in their sale to the Western Milling ESOP Trust