Industry Trends

Largest Transactions Closed

- Target

- Buyer

- Value($mm)

Last updated:

In an M&A transaction, one major sticking point is how the deal should be structured: as an asset sale or a stock sale? Buyers and sellers often find themselves on opposing sides for legal and tax reasons. Finding a transaction structure that is acceptable to both is key to a successful transaction.

One often-cited solution to this problem is the section 338(h)(10) election, which permits the transaction to be treated as a stock sale for legal purposes and as an asset sale for tax purposes. But inherent limitations in the Internal Revenue Code make this approach somewhat risky. A section 368(a)(1)(F) reorganization (F-reorganization), on the other hand, provides flexibility that benefits both the buyer and the seller—while avoiding the limitations imposed by the 338(h)(10) election.

Here’s why the F-reorganization is an excellent tool for finding compromise when you are structuring an M&A deal as a stock sale.

When all else is equal, buyers typically prefer an asset sale. It gives them a stepped-up tax basis in the target company’s assets, which provides accelerated depreciation expenses—allowing them to reduce future taxable income. But sellers typically would oppose an asset sale. Why? If you’re an S corporation or LLC, you would be taxed at the higher ordinary income tax rate. If you’re a C corporation, the news is even worse—you would be subject to double taxation: the company pays capital gains on the assets sold, and then the selling shareholders pay income tax on distributions.

That’s why, as a seller, you likely would prefer a stock sale. It lets you either avoid double taxation (C corporation) or receive preferential capital gains treatment compared with income tax (S corporation or LLC). For this reason, the 338(h)(10) election often appears useful from the seller’s perspective. Sure, it would be beneficial to you for tax purposes—but let’s take another look.

Under section 338(h)(10) of the Internal Revenue Code, the parties involved in the sale of an S corporation can jointly choose to make this election, which seems to benefit both the seller (as a stock sale for legal purposes) and the buyer (as an asset sale for tax purposes). While a stock sale is also beneficial to the seller for tax purposes, the 338(h)(10) election mostly benefits the buyer by reducing future taxable income as described above. Since the transaction is legally a stock sale—with no change to the legal entity—this structure avoids issues surrounding change of control or contract assignability that may come up in an asset sale.

The 338(h)(10) election may seem like a win-win structure, but depending on your situation, it may pose difficulties due to its innate limitations, including the following:

When structuring a 338(h)(10) election, consulting legal counsel and tax advisors—who will perform due diligence and analysis to ensure compliance with these requirements—is a must. Significant focus will be placed on the target company’s S corporation status, and all parties involved in the transaction have a stake in confirming that status. If the target company’s S corporation election was inadvertently invalidated at some point, the company would in fact be a C corporation, and thus would not be permitted to make the 338(h)(10) election.

To mitigate the limitations and risks characteristic of a 338(h)(10) election, therefore, M&A professionals will often recommend structuring the transaction as an F-reorganization instead.

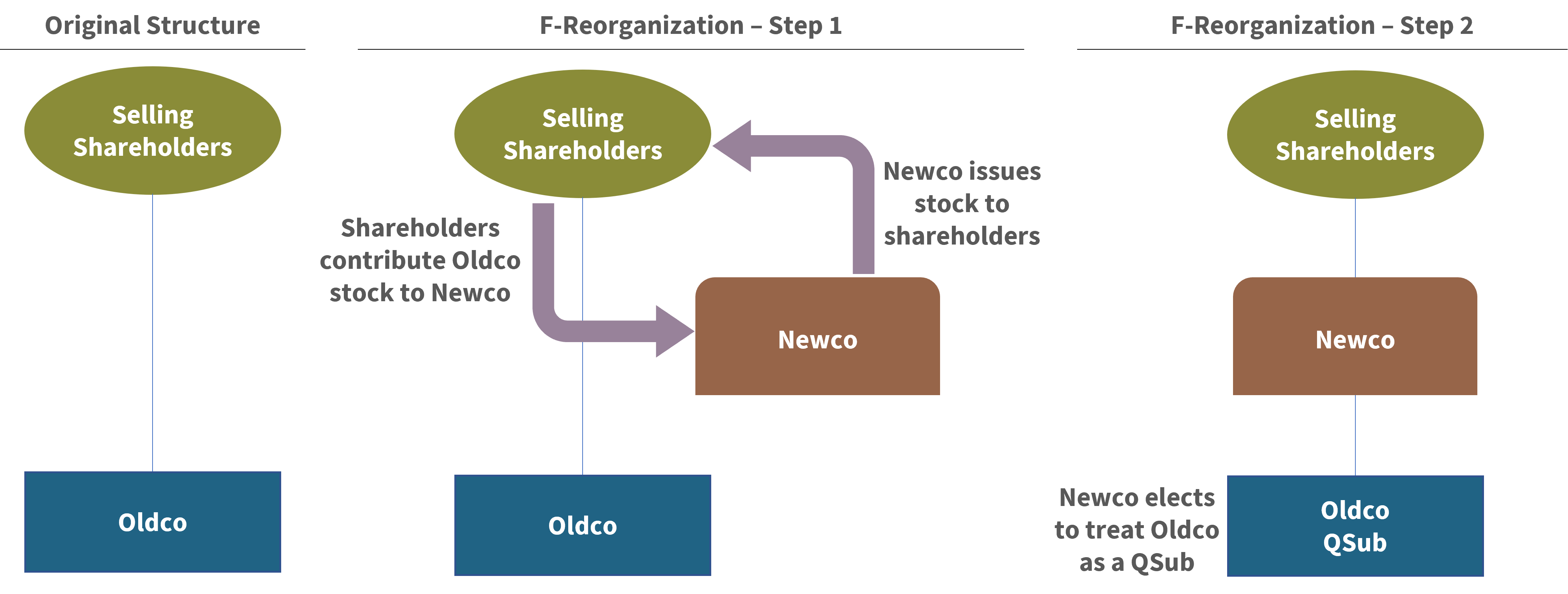

An F-reorganization under section 368(a)(1)(F) of the Internal Revenue Code is defined as “a mere change in identity, form or place of organization of one corporation, however effected.” The primary benefit for buyers is that an F-reorganization allows them to step up their tax basis in the target company’s assets without requiring the target to maintain its S corporation status. And you get to move forward with the stock sale, which generally is preferred by sellers (as described above).

F-reorganization is a two-part process:

The F-reorganization allows the buyer to receive the step-up in tax basis on Oldco’s assets, even if the buyer acquires less than 80% (which is not permitted in a 338(h)(10) election).

Private equity investors often require an equity rollover, which is when selling shareholders retain a portion of ownership in the company post-transaction. Under the 338(h)(10) election, the equity rollover is limited to a maximum of 20% of the pre-transaction equity. But the F-organization allows the selling shareholders to defer tax on the portion rolled over.

Furthermore, an F-reorganization is particularly beneficial in private equity transactions where the buyer (typically an LLC) seeks to acquire an S corporation. S corporations must be owned by actual individuals and cannot be owned by an LLC, and converting an S corporation to an LLC is usually considered a taxable liquidation. Since the F-reorganization involves electing the Oldco QSub (an S corporation) as a disregarded entity for tax purposes, however, the Oldco QSub may be converted to a single-member LLC without federal tax consequences. LLCs have fewer shareholder limitations, and other LLCs can be shareholders. This added benefit is not available through a 338(h)(10) election, which adds to the F-reorganization’s popularity with private equity investors or other LLC acquirers.

***

As a tool for compromise when structuring an M&A deal, the F-reorganization benefits both the buyer and the seller—and avoids the restrictions of the 338(h)(10) election. The seller reaps tax benefits from the transaction being structured as a stock sale. The buyer benefits from a decrease in future taxable income. Every transaction and tax situation are unique, however, so it’s critical to seek guidance from legal counsel and tax advisors when structuring an F-reorganization.