Industry Trends

Largest Transactions Closed

- Target

- Buyer

- Value($mm)

Advised Western Milling in their sale to the Western Milling ESOP Trust

Last updated:

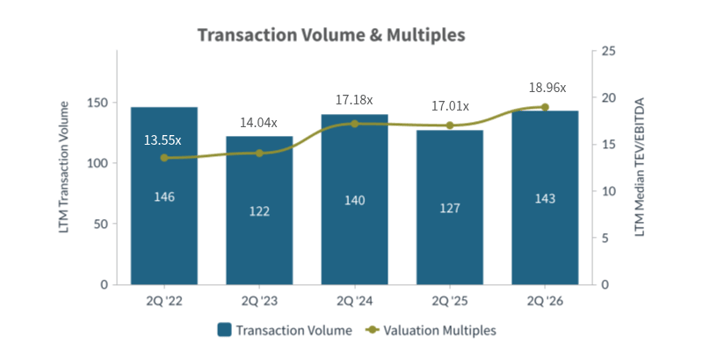

Valuation appetite strengthened into Q2 2026, with 143 LTM transactions (36 in Q2) at median multiples of 18.96× TEV/EBITDA and 4.09× TEV/Revenue — the highest revenue multiple in the trailing four-year lookback. Buyers competed intensely for defense electronics, mission-critical manufacturing, space systems, and sustainment assets. Commercial aerospace aftermarket demand remained durable amid persistent OEM delivery backlogs, while defense procurement urgency accelerated around FY2026 budget priorities including missiles, munitions, and missile defense. Key transactions included TransDigm/Victor Sierra Aviation, VSE/Precision Aviation Group, and Howmet/Consolidated Aerospace Manufacturing.¹ ³

“The Aerospace, Defense & Government Contracting sector continues to reward companies with differentiated, mission-aligned capabilities,” said David Jasmund, Managing Director at PCE. “Buyers are not just acquiring revenue — they are acquiring access: to cleared workforces, established contract vehicles, and proprietary technology that is difficult to replicate. Owners who understand that distinction enter the market with a significant advantage.”

Q2 2026 posted 36 deals; LTM volume reached 143 (vs. 127 a year prior) at median multiples of 18.96× EBITDA and 4.09× revenue — the highest revenue multiple in the trailing four-year lookback. Defense procurement urgency, commercial aerospace aftermarket demand, and emerging space sector activity drove buyer sentiment. Strategics pursued vertical integration while financial sponsors prioritized O&M-weighted platforms with recompete certainty and CMMC readiness.¹ ² ³ ⁶

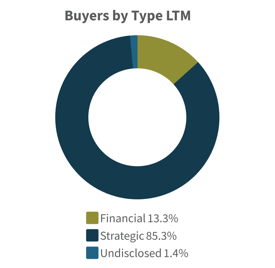

Strategic Acquirers: 1122 of 143 LTM deals (85.3%) — activity concentrated in aerospace MRO, defense electronics, space systems, autonomous/UAS platforms, and mission-critical manufacturing. Strategics competed intensely for proprietary technology, cleared workforces, and vertical integration targets across defense and commercial aerospace.1 3

Financial Buyers: 19 of 143 LTM deals (13.3%) — sponsors focused on platform carve-outs, precision aerospace components, avionics/MRO, and defense services. Deal selection emphasized durable cash flow, task-order recompete visibility, and CMMC compliance as baseline underwriting criteria.1 3

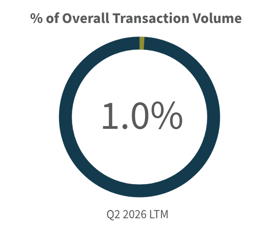

Aerospace, Defense & Government Contracting posted 143 LTM transactions (36 in Q2) against 14,857 total U.S. M&A deals, representing approximately 1.0% of overall volume and 1.1% of Q2 activity. The sector’s relative share reflects structural insulation from broader market cyclicality, underpinned by defense budget tailwinds, NDAA-driven procurement, and growing space sector deal flow. Buyer conviction strengthened further into mid-2026 as strategics and financial sponsors competed for mission-critical platforms.1 3 6

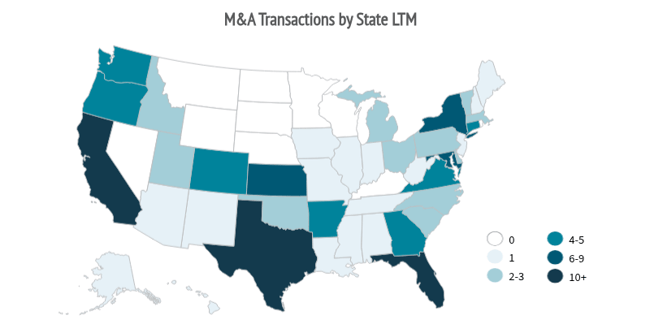

Seller activity led by California (24), Florida (17), Texas (11), Maryland (7), and New York (7), reflecting dense aerospace manufacturing footprints, DoD installations, and cleared-labor ecosystems that align with buyer preference for established defense corridors.

Notable Q2 activity in California and Florida was driven by aerospace MRO and manufacturing consolidation, while Texas and Maryland continued to anchor defense electronics and government services deal flow.

| Target | Buyer | Value ($mm) |

| Victor Sierra Aviation Holdings LLC/Jet Parts Engineering, LLC | TransDigm Group Incorporated | $2,200 |

| Precision Aviation Group, Inc. | VSE Corporation | $2,150 |

| Consolidated Aerospace Manufacturing, LLC | Howmet Aerospace Inc. | $1,800 |

| Mistral, Inc. | Ondas Inc. | $175 |

| World View Enterprises, Inc. | Ondas Inc. | $136 |

| Aircraft Reconfig Technologies LLC | AAR Aircraft Services, Inc. | $35 |

| A & B Aerospace Inc. | PMGC Holdings Inc. | $5 |

| Unical Aviation Inc. | Satair USA Inc. | n/a |

| Target | Buyer | Value ($mm) |

| Genesys Industries, Inc | Greybull Stewardship LLC | n/a |

| International Aerospace Coatings, Inc. | H.I.G. Capital, LLC | n/a |

| Stratton Aviation, LLC | Industrial Opportunity Partners, LLC | n/a |

| Maine Aviation Corporation | Black Forest Ventures LLC | n/a |

| Target | Buyer | Value ($mm) |

| Space-ng Inc. | Firefly Aerospace Inc. | n/a |

| North Star Scientific Corporation | Global Air Logistics and Training, Inc. | n/a |

| Futuramic Tool & Engineering LLC | Advanced Integration Technology, LP | n/a |

| Aero Controls, Inc. | Air Transport Components, LLC | n/a |

| Exquadrum, Inc. | Mach Industries Inc. | n/a |

Source S&P Capital IQ as of 7/1/2026 and PCE Proprietary Data

Defense procurement momentum is expected to remain elevated into Q3, supported by Golden Dome missile defense, shipbuilding, autonomous systems, and space sector expansion, while commercial aerospace aftermarket and MRO remain structurally well-positioned as OEM delivery delays persist. Key risks include government budgeting uncertainty, continuing resolution delays, cleared-workforce constraints, and CMMC compliance timelines that may compress valuations for non-certified suppliers.1 3 5 6

David Jasmund |

Michael Rosendahl |

Eric Zaleski |

Advised Western Milling in their sale to the Western Milling ESOP Trust