Industry Trends

Largest Transactions Closed

- Target

- Buyer

- Value($mm)

Advised Western Milling in their sale to the Western Milling ESOP Trust

Last updated:

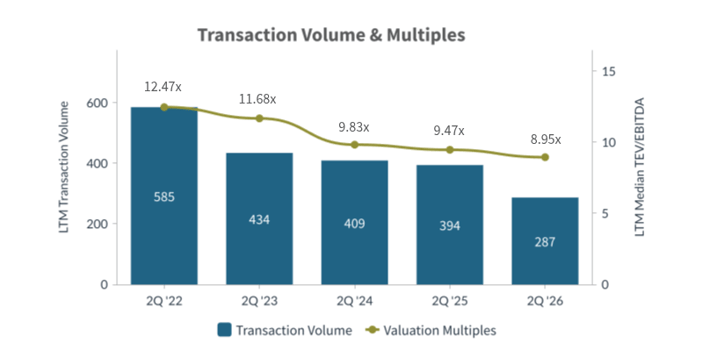

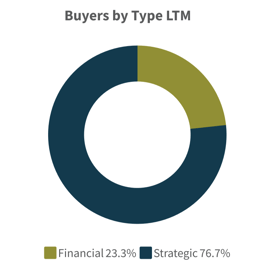

M&A activity in the Food & Agriculture sector continued its downward trajectory in Q2 2026, with 287 closed transactions (LTM), down from 394 in Q2 2025 and 585 at the Q2 2022 peak. Valuation multiples declined further, with the median TEV/EBITDA at 8.95x and TEV/Revenue at 1.28x, reflecting sustained investor caution amid margin compression and ongoing cost pressures. Strategic buyers led the market, comprising 77% of deal activity, while financial buyers accounted for 23% — a rising share as sponsors pursued branded and growth-oriented targets. Despite a softer volume environment, select high-value transactions highlight continued appetite for scaled assets in beverage, distilled spirits, and health-oriented food categories.

"Strategic acquirers continue to set the tone in Food & Agriculture M&A, but we're seeing a meaningful shift as financial sponsors grow more active in pursuing branded, consumer-facing platforms," said Michael Poole, Managing Director at PCE Investment Bankers. "Owners who understand which buyer type is best suited to their business will be better positioned to maximize value in this environment."

Valuation pressures intensified in Q2 2026 as deal volume fell to 287 LTM transactions — a multi-year low — and multiples contracted across the board. Median TEV/EBITDA declined to 8.95x (from 9.47x in Q2 2025 and 12.47x at the Q2 2022 peak), while TEV/Revenue compressed to 1.28x, down from 1.42x. Buyers continued to prioritize earnings quality and operational resilience over top-line scale, with premium valuations reserved for assets offering strong brand equity, vertical integration, or defensible distribution in health, beverage, and specialty food categories.

Strategic Acquirers: Strategic buyers dominated Q2 2026 activity, comprising 77% of transactions (220 of 287). Key acquisitions included Refresco's $1.22B purchase of SunOpta and E. & J. Gallo Winery's $775M acquisition of Four Roses Distillery, reflecting continued interest in beverage scale and premium spirits integration.

Financial Buyers: Financial buyers accounted for 23% of deal volume — a notable increase from prior periods — focusing on branded, health-oriented, and specialty food assets. Notable investments included ACON Investments' backing of Yummy Earth and Hoffmann Family of Companies' acquisition of Cedar Crest Specialties, underscoring sponsor interest in consumer-facing brands with growth runway.

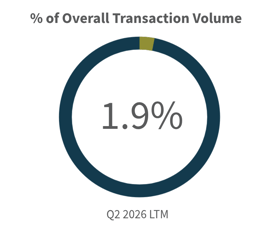

The Food & Agriculture sector continued to underperform high-growth verticals such as technology and healthcare but demonstrated relative resilience compared to cyclical sectors including retail and discretionary consumer goods. With LTM deal volume declining to 287 transactions in Q2 2026 — representing approximately 1.9% of overall M&A activity — the sector reflects broader market caution while still attracting capital into defensive, essential-use, and health-aligned food assets. Premium valuations remain achievable for scaled platforms in beverage, specialty food, and agricultural technology, where strategic scarcity and GLP-1 tailwinds are driving buyer interest.

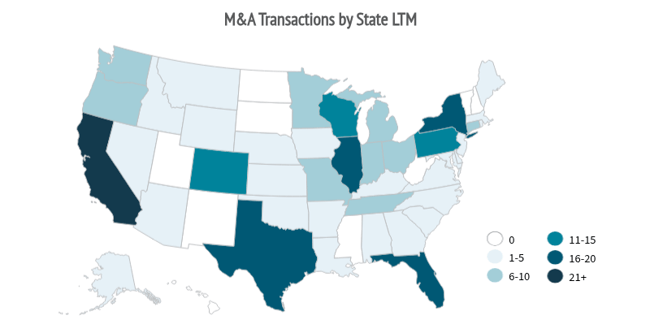

Top U.S. States: California led with 55 transactions, followed by Illinois (18) and Texas (18), underscoring their concentration of food producers, processors, and consumer brand headquarters.

Cross-Border Trends: Cross-border appetite remained active, with international buyers — particularly from Europe and Asia-Pacific — targeting U.S. food, beverage, and specialty agricultural assets for brand diversification and market access.

| Target | Buyer | Value |

| SunOpta Inc. | Refresco B.V. | $1,220 |

| Four Roses Distillery LLC | E. & J. Gallo Winery, Inc. | $775 |

| Calavo Growers, Inc. | Mission Produce, Inc. | $492 |

| Bachan's, Inc. | The Marzetti Company | $400 |

| Black Buffalo Inc. | Imperial Brands PLC | $150 |

| The Mochi Ice Cream Company, LLC | Morinaga&Co., Ltd. | $130 |

| Farmer Bros. Co. | Royal Cup, Inc. | $88 |

| SRx Health Solutions Inc. | SRX Global Inc. | $82 |

| Terrasoul Superfoods, LLC | Laird Superfood, Inc. | $53 |

| Eaze, Inc. | Vireo Growth Inc. | $49 |

| Target | Buyer | Value |

| Oakbio, Inc. | Biosphere Inc., United States | n/a |

| Wyoming Whiskey, Inc. | WW Partners, LLC | n/a |

| The New Bar, Inc. | The Zero Proof LLC | n/a |

| Floyd County Brewing Company | Upland Brewing Company | n/a |

| Clearwater Seed Inc | Millborn Seeds, Inc. | n/a |

| Target | Buyer | Value |

| Yoerg Brewing Company LLC | Undisclosed | n/a |

| Yummy Earth, Inc. | ACON Investments, L.L.C.; The Fini Company | n/a |

| Cedar Crest Specialties, Inc. | Hoffmann Family of Companies | n/a |

| Masi Masa Trading Company LLC | Poolhouse Technologies Ltd | n/a |

| Pyramids Pharmacy Inc. | Great Point Partners, LLC | n/a |

Source S&P Capital IQ as of 7/2/2026 and PCE Proprietary Data

Opportunities: AgTech platforms with demonstrated AI applications in precision farming and supply chain optimization are well-positioned to attract both strategic and financial buyers, as operators seek productivity gains to offset compressed margins.³ Functional food and high-protein CPG brands aligned with GLP-1 dietary behaviors represent strong bolt-on targets for large strategics looking to reposition legacy portfolios.5

Risks: The lagged pass-through of 2025 tariff escalations is projected to hit consumer food prices between April and October 2026, compressing margins across labor-intensive processing and manufacturing models and potentially cooling mid-market deal appetite.¹ Ongoing trade policy uncertainty — particularly with China, where U.S. ag exports collapsed— adds a further layer of unpredictability to cross-border deal structures.2

Predicted Activity: Expect continued consolidation in domestic commodity processing and ag inputs as buyers pursue supply chain insulation. Roll-up activity in functional food, protein snacks, and health-oriented beverage brands should accelerate through Q3 2026, driven by GLP-1 tailwinds and strategic portfolio repositioning.5

David Jasmund |

Michael Poole |

Will Stewart |

Advised Western Milling in their sale to the Western Milling ESOP Trust